- Edit

- 23A TANNERY PARK, 21 BELMONT RD,

Cape Town,Western Cape - 7700 - 021 794 4329

- http://www.belmontasset.co.za/

- Send Inquiry by Email

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

About company

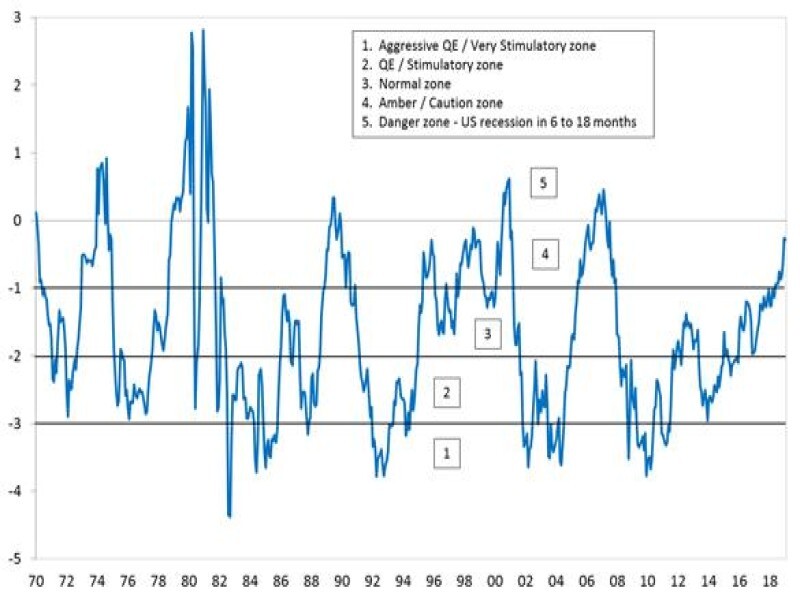

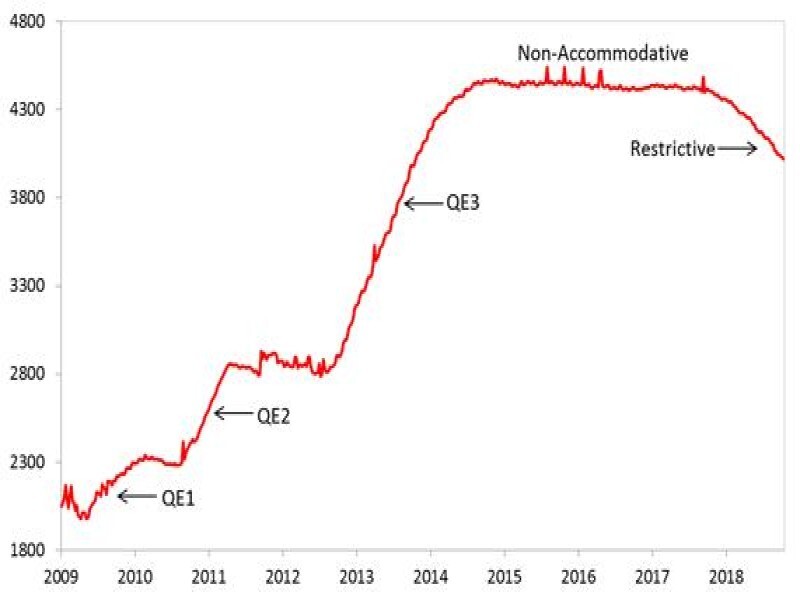

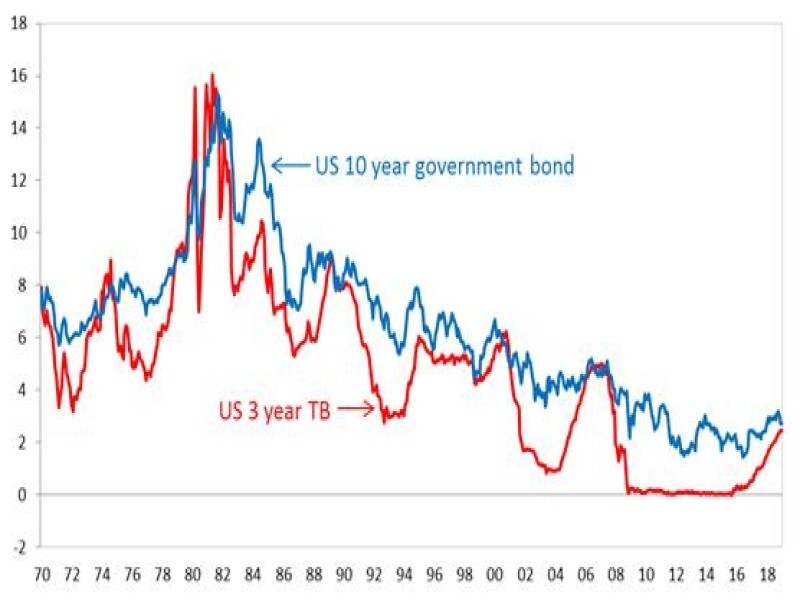

A feature of the past quarter was the sudden capitulation of global economic growth expectations and sharp downward corrections in economically sensitive asset prices such as shares and oil. The dominant force at play appears to have been US monetary policy which became excessively tight relative to prospective growth and inflation but ongoing tariff wars no doubt played a role too. Tighter US monetary policy (chart 1) was a consequence of the Fed’s oft-stated intention to normalise the term structure of US interest rates (known as the “yield curve”). Aggressive quantitative easing (QE) following the global financial crisis of 2008 created downward distortions in interest rates, especially short-term rates (chart 2):

Hours :

Hours not available. Please contact Belmont Asset Management (Pty) Ltd at 021 6853724.

Is this your business?

Recommended Reviews for Belmont Asset Management (Pty) Ltd

People also viewed

Mergence Investment Managers 0 Reviews

Ltd")

Belmont Asset Management (Pty) Ltd 0 Reviews

Ginsberg Financial Brokerage 0 Reviews